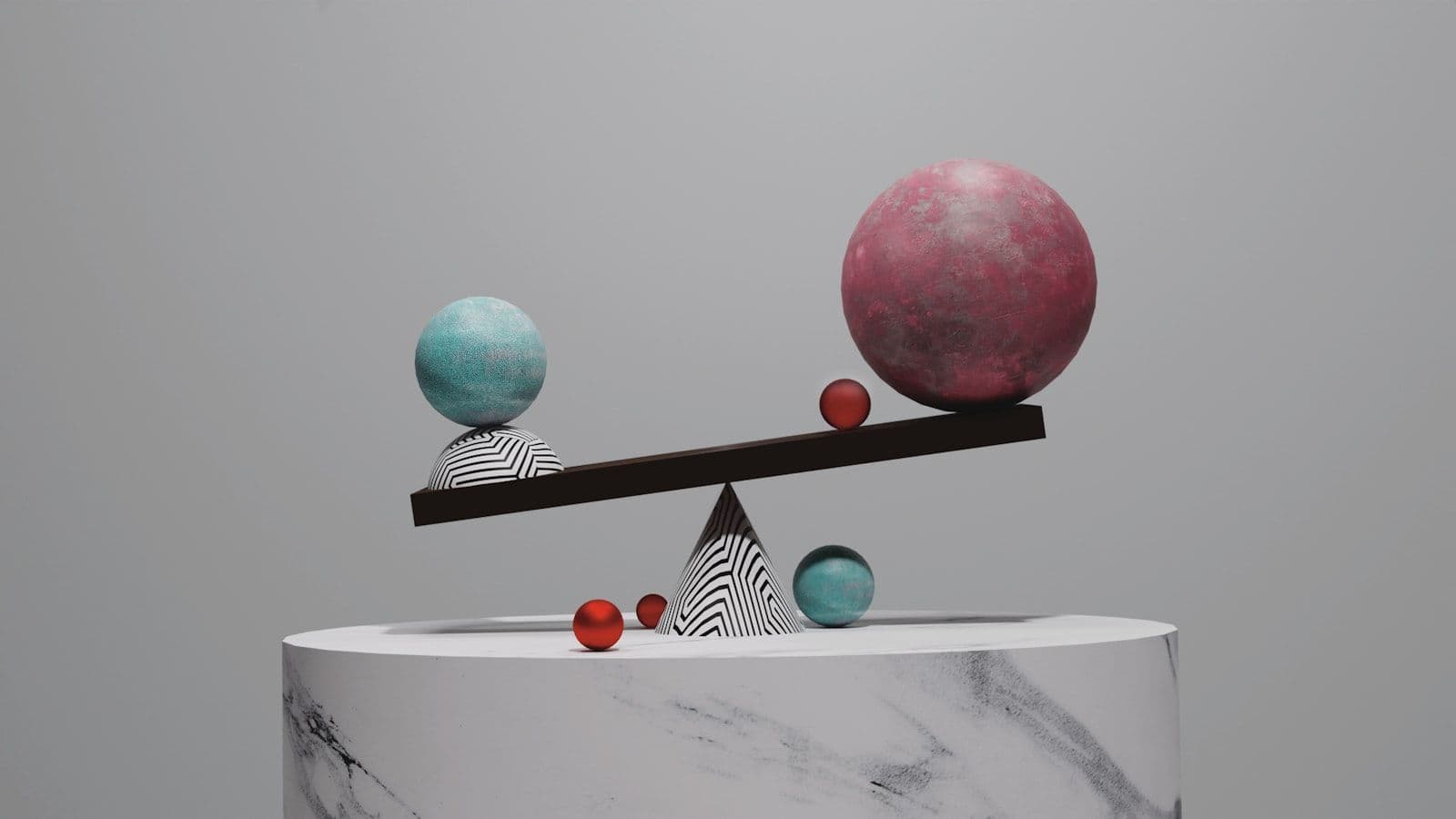

Five factors determine a FICO credit score: payment history at 35 percent, amounts owed at 30 percent, length of credit history at 15 percent, new credit at 10 percent, and credit mix at 10 percent. Payment history and amounts owed together drive roughly two-thirds of the score, which is why they receive the most attention.

These weights come from the FICO scoring model used by most lenders. FICO publishes the five category percentages for the general population, but the precise weighting shifts for each individual profile based on the information in the file, so the same action can move two people's scores by different amounts.

This article explains the standard FICO model weights and how each factor behaves. It does not cover VantageScore or industry versions such as FICO Auto, both of which are compared in the guide on FICO versus VantageScore.

Key takeaways

- Payment history is the single largest factor at 35 percent of a FICO score.

- Amounts owed, driven mostly by credit utilization, accounts for 30 percent.

- Length of credit history contributes 15 percent and rewards older, well-aged accounts.

- New credit and credit mix each contribute 10 percent of the total score.

- The two largest factors are also the most controllable in the short term.

- FICO weights are population averages and shift based on the data in each individual file.

Why is payment history the most important factor?

Payment history measures whether obligations were paid on time, and at 35 percent it carries more weight than any other factor. A consistent record of on-time payments is the strongest signal a scoring model uses to predict future repayment, so even a single missed payment can have an outsized effect on the score. The factor accounts for payments across every account type, including cards, mortgages, auto loans, and student loans, and it also reflects how severe and how recent any late payments were, so a 90-day delinquency weighs more than a 30-day one.

A payment reported 30 days late can lower a score significantly, and the mark reports for seven years from the delinquency. When a late payment is reported in error, the correction process is described in the article on how to remove late payments. Recency also matters, because a recent late payment weighs more heavily than an old one.

How do the five factors compare by weight?

The five factors are not equal. Payment history and amounts owed dominate, while the remaining three share the final third of the score. The table below shows each factor, its standard weight, and what it measures, which helps clarify where attention produces the largest return.

| Factor | Weight | What it measures |

|---|---|---|

| Payment history | 35% | Whether payments were made on time across all accounts |

| Amounts owed | 30% | Total balances and the credit utilization ratio |

| Length of credit history | 15% | Average and total age of credit accounts |

| New credit | 10% | Recent applications and newly opened accounts |

| Credit mix | 10% | Variety of revolving and installment accounts |

These percentages describe the general population, not any one person. For someone with a thin file or a recent bankruptcy, the model may lean more heavily on certain categories, so the published weights are best read as a guide to priorities rather than a fixed formula.

How much does credit utilization affect a score?

Credit utilization, the share of available revolving credit in use, is the largest part of the amounts-owed factor. Keeping utilization low is one of the fastest ways to support a score, as detailed in the guide on credit utilization.

- Utilization under 30 percent is a common benchmark, and under 10 percent is stronger still.

- Both per-card and overall utilization are evaluated by scoring models.

- Utilization is recalculated each month, so improvements can appear quickly.

Because utilization is recalculated with each statement, it is one of the few factors that can change a score within a single billing cycle. Paying a balance down before the statement closing date, rather than the due date, is what determines the figure that gets reported to the bureaus. There is no carryover memory for utilization either, so a high ratio one month does not haunt a file once the balance is paid down, which makes it one of the most forgiving factors to manage.

Does the length of credit history matter?

Length of credit history contributes 15 percent and considers the age of the oldest account, the average age of all accounts, and how long specific accounts have been active. Older accounts demonstrate a longer track record of management, which a scoring model reads as lower risk.

This is why closing an old card can work against a profile. It can lower the average age of accounts over time, and it reduces total available credit, which raises utilization on the accounts that remain. A long-held account with no annual fee is usually worth keeping open even when it sees little use. A closed account in good standing can still report for up to ten years, so the effect on average age is gradual rather than immediate, but the loss of available credit shows up in utilization right away.

How do new credit and hard inquiries affect the score?

New credit makes up 10 percent and reflects recent applications and newly opened accounts. Each application can generate a hard inquiry, though the score impact is usually small and temporary, as explained in the article on whether hard inquiries hurt a credit score.

Opening several accounts in a short window can signal elevated risk and lower the average age of accounts at the same time. Rate shopping for a single loan within a focused window is typically grouped into one inquiry for scoring purposes, so comparing mortgage or auto offers does not multiply the impact.

What is credit mix and how much does it count?

Credit mix is the final 10 percent and rewards experience managing different account types, such as revolving credit cards and installment loans. The composition of a profile is broken down in the guide on credit mix.

Credit mix is a minor factor, and opening an account purely to diversify rarely makes sense given the cost and the inquiry involved. It tends to improve naturally as a borrower takes on different products over time, such as a first auto loan or mortgage alongside existing cards.

Skip the paperwork. Lock in your spot.

CreditRefresh drafts your FCRA dispute letter and tracks the 30-day investigation window. You review, approve, and send. You stay in control.

Lock in your spotWhich factors can be improved fastest?

The amounts-owed and payment-history factors respond most quickly to action, because both update with each reporting cycle. A practical sequence appears in the guide on how to improve a credit score. The steps below order the highest-impact moves first.

- Bring any past-due accounts current to stop new late marks from being reported.

- Pay down revolving balances to lower utilization before the statement closing date.

- Avoid new applications that are not necessary, limiting fresh hard inquiries.

- Keep older accounts open to preserve account age and total available credit.

- Dispute any inaccurate negative items that are dragging the score down unfairly.

Do all lenders use the same FICO weights?

Not exactly. The 35, 30, 15, 10, 10 breakdown describes the general-purpose FICO model, but lenders may use industry-specific versions or a different score entirely. The Consumer Financial Protection Bureau explains the range of scores in circulation at consumerfinance.gov.

Auto lenders and card issuers often use tailored models that weigh certain behaviors differently, which is why a single consumer can hold several scores at once. General guidance on understanding and protecting a score is available from the Federal Trade Commission at consumer.ftc.gov.

What is not counted in a credit score?

Several pieces of information that consumers expect to matter are excluded from FICO scoring entirely. Income, employment, age, and similar factors do not appear in the score, even though a lender may consider them separately when deciding whether to approve an application. The score is built only from the information in the credit report itself, which is why two people with very different salaries can hold identical scores, and why a raise at work does nothing to move the number on its own.

- Income, savings, and bank account balances are not part of any FICO score.

- Age, marital status, and similar demographic details are excluded by law from scoring.

- Checking a personal credit report is a soft inquiry and never lowers a score.

Does carrying a balance help a credit score?

No. Carrying a balance from month to month does not help a score, and it adds interest cost for no scoring benefit. This is one of the most persistent myths in personal finance, and it leads many consumers to pay interest unnecessarily in the belief that it builds credit.

What the model rewards is on-time payment and low utilization, both of which are satisfied by paying a statement in full. A card used regularly and paid off each month reports active, responsible use without any interest charge, which is the ideal pattern for the payment-history and amounts-owed factors.

The confusion likely comes from the fact that an active account reports more useful data than a dormant one. Activity matters, but a revolving balance left unpaid is not what creates that signal, so there is no scoring reason to avoid paying a card in full.

How can a consumer see which factors are hurting a score?

Most free credit-score tools list the top factors affecting a score, often phrased as reason codes such as high utilization or a recent missed payment. Reading these codes points directly to which of the five factors is dragging the number down at any given time.

Pairing those reason codes with a full review of all three credit reports gives the clearest picture. The codes explain the why, while the reports show the specific accounts behind them, and together they let a consumer focus effort on the factor with the largest current impact rather than guessing.

Why do credit scores differ across the three bureaus?

A consumer often sees three different scores because each bureau may hold slightly different data. A lender might report to only one or two bureaus, an account might appear on one file but not another, and the timing of updates can vary, so the same five factors are calculated on slightly different inputs.

These differences are normal and rarely large. The more important point is that the same behaviors, on-time payments and low utilization, strengthen the file at every bureau, so working the underlying factors improves all three scores rather than chasing one number in isolation.

Frequently asked questions about credit score factors

What is the most important factor in a credit score?

Payment history is the most important factor, making up 35 percent of a FICO score. A consistent record of on-time payments has a larger effect than any other single category, and recent late payments weigh more heavily than older ones, so keeping current accounts on time is the foundation of a strong score.

What credit utilization ratio is best for a score?

A utilization ratio under 30 percent is a widely cited benchmark, and keeping it under 10 percent is stronger still. Utilization is recalculated monthly, so paying balances down before the statement closing date, rather than the due date, can improve the reported figure within a single billing cycle.

Does closing a credit card lower a score?

It can. Closing a card removes available credit, which raises utilization on the remaining accounts, and over time it can lower the average age of accounts. Both effects can reduce a score even when the closed card carried no balance, which is why long-held no-fee cards are usually worth keeping open.

How long does it take to improve a credit score?

Utilization changes can appear within one or two billing cycles, while rebuilding payment history takes considerably longer. There is no fixed timeline, and outcomes depend on the specific items affecting the profile and how recent they are, so two people taking the same steps may see different results. As a general pattern, the negative weight of a late payment or collection fades gradually as the item ages, even before it falls off entirely.

Do the five factors apply to VantageScore too?

VantageScore uses similar inputs but describes and weights them differently, and it can score a thinner file than FICO requires. The five-factor percentages discussed here apply to the standard FICO model, not to VantageScore or to industry-specific scoring versions used by some auto and card lenders.

Last reviewed: June 2026

This article is for educational purposes only and does not constitute legal or financial advice. The Fair Credit Reporting Act and related regulations are complex, and outcomes depend on individual circumstances. Consumers with specific questions about their credit reports or rights under federal law should consult a licensed attorney or contact the Consumer Financial Protection Bureau directly.